Investing with Franz Kafka and John Bogle

|

|---|

| Dedicated to the 100th anniversary of Franz Kafka’s death |

Franz Kafka died of tuberculosis on June 3, 1924, when he was only 40 years old. He would have turned 41 a month later.

A writer who was unknown at the time and worked for a living in an insurance company, Generali, today one of the largest Italian companies but which at the time was part of the Austro-Hungarian kingdom, since Trieste until WW1 belonged to Austria (Kafka himself spoke German and all his works are in German).

“Please burn everything”, these were Kafka’s requests to his closest friend when he was close to death, he believed he was a bad writer…. All his life no one made him believe the opposite.

|

|---|

| I personally took this photo of Kafka’s statue in Prague, his birthplace |

Only after his death he will receive the glory he deserves, which still lasts today. At Christmas 2023 I got myself a small book, “Metamorphosis”, which I finished in just 2 hours, because it was interesting, and made him one of my favorite writers.

John Bogle was born in 1929, five years after Kafka’s death, so the two could never have met physically. In my opinion, however, the 2 of them could have shared some ideas about the way of reasoning, and in this creative review I will try to merge the two ideologies into a possible financial worldview.

Who is John?

John Bogle was a benefactor, God himself, the creator of humanity… no okay, I’m just exaggerating.

|

|---|

| John is the creator of Vanguard Group |

Before Vanguard, investing in indexes (e.g. S&P500) was very complicated, no one offered you a ready-made ETF to

buy in the market, and you had to basically buy every stock by hand and rebalance on your own when needed.

At that time (1970s) mutual funds offered only active investments with high fees and over the long term they

underperformed the indexes (active funds still do today, looking at their historical data).

Vanguard practically created passive investing, which over the long term (20+ years) so far has always had

better results because of the extremely low fees.

Vanguard’s structure is different because unlike competitors such as Blackrock, there are no shareholders to account

for profits (e.g. from annual fund fees, the Total Expense Ratio).

Vanguard is not publicly traded, but its shares are included within the funds themselves: if you buy an ETF from

Vanguard, automatically a small portion of Vanguard will be yours.

Ideally, Vanguard is serving the interests of the investors themselves, and fees are expected to be reduced because of

the profits from its products

(e.g. 2022).

Nowadays, 2024, Vanguard handles 8.6T$

in assets for their customers. When Jogn died, in 2019, they were approximately 6T$ (a.k.a. 6,000 billions).

What am I trying to say? Today everyone knows Warren Buffett, one of the richest men in the world, yet he manages

less than $1T, he ate a big piece of the pie.

When Bogle died in 2019, despite the fact that his fund company managed such high assets, he personally held

only $80 million (0.05% of Warren Buffett’s $139 billion today).

Besides never becoming a billionaire and benefiting many people when he was alive, Bogle decided to donate everything to

charity in his will.

Simple is better

Kafka’s language is simple, immediate, straight to the point.

He is able to create an absurd story but keeping it plausible and without exaggeration.

This idea fits well with John’s suggested passive investment strategy: take only one ETF (U.S. or All World)

and hold it for as long as possible.

A simple strategy, but one that has proven to be the most effective over time because of its extremely low fees and

the reliable replication of the index.

Don’t buy the needle in the haystack, buy the haystack ~ John C. Bogle

The best advice is to avoid expensive funds that invest in particular niches, they have high fees and the expected

returns are not necessarily higher.

By investing on a global index, we have confidence that over the long term (tens of years), the global wealth will

increase (in the past the average has been 7% per year), one year may very well go wrong, but it doesn’t concern us.

Doing market timing can be very dangerous: if tomorrow my investment increased, I would still hold it for tens of years,

since that is my goal.

Betrayal

Market

To get the best performance in the long run, just select the companies that will perform best.

Thanks… But we don’t have a crystal ball, and no one can predict the future (not even a financial analyst

paid millions).

If someone tries to convince you otherwise, they want your money.

Or it’s someone really skilled like Jim Simons (rip), who does High Frequency Trading and gets +50% a year,

but he has nothing to do with investing in companies, he exploits temporary market inefficiencies, and his Medallion

Fund is not even open to everyone.

Targeting individual stocks is therefore counterproductive: we are at the mercy of the financial performance of individual companies and on average we will do worse than we would have done by investing directly in an index, without wasting hours on analyzing financial statements.

We don’t have to play as if we are at a casino: by buying the whole market we expect that on average the global wealth

will grow and this will directly benefit us, who own a part of those who produce this wealth.

Companies are not just abstract concepts, there are people behind them, and by investing in them, we own a part of it,

which ideally will accumulate value over time.

Active funds

We can beat the market, give us your money

Active funds manage to turn a winning strategy into a favorable game for them, so they can squeeze out the inexperienced people who trust them.

|

|---|

| Performance of active funds in the long term |

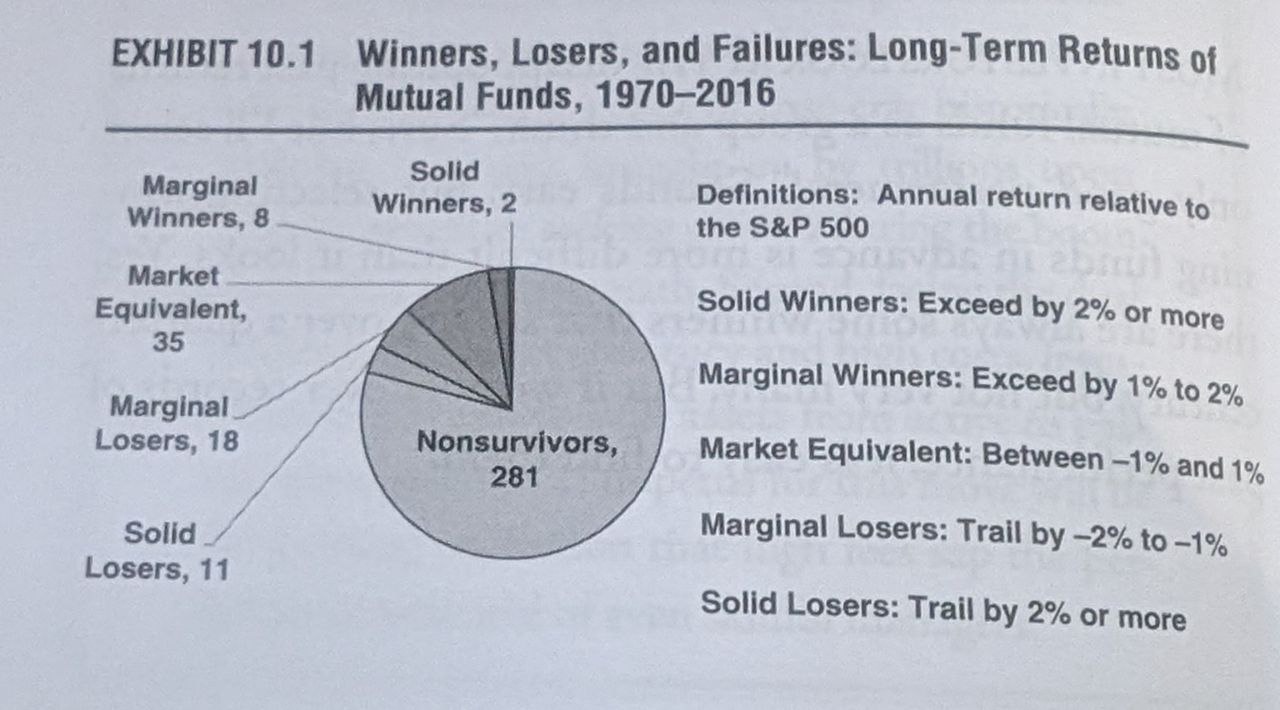

Here is an image extracted from John Bogle’s book regarding the performance of active funds tracking the U.S. market,

which were present in 1970 and checked after 46 years (2016).

Out of 355 funds in total, as many as 281 (~80%) shut down over time, due to various factors (poor performance,

business decisions, etc.) and investors were forced to look elsewhere…

Of those that survived, only 2 significantly beat the S&P500 (0.5%), so basically the percentages of catching the

right one were zero.

BEWARE, this chart doesn't consider fees, those who invested in an active fund also paid more of them, so in addition

to doing worse than the market, we paid the fund manager more to allow us to do worse than the market.

Absurd fees of active funds

As we have just seen, the promise we are given when we want to invest is that in an active fund there are some super

experts who enable us to achieve superior performance, and rightly they want their reward, which is a higher % of fees.

There is just one small problem…. The vast majority do worse than the market, and with the fact that the fees are significantly higher, those who decide to invest in the fund lose additional money, getting a double robbery.

In fact, one only has to read the fund’s prospectus to see that management fees are usually around

2 - 3% of our invested amount, each year, for a fund that performs worse than the market as a whole.

In contrast, buying an ETF that covers the entire U.S. market allows us to get the same performance as the market

(which is higher than the vast majority of active funds) and is much cheaper, in the European market an ETF

that physically replicates the S&P500 costs just 0.03% per year.

Financial promoter

Like Gregor who is initially a slave to his job to support his family, the financial promoter who works for a bank is

willing to tell you anything to gain more commission from the products he sells.

In fact, his job allows him to directly get a % of the amount you invest by selling certain products created by his bank

that are certainly not in your favor (maybe someone said conflict of interest?).

The problem is that he has also convinced himself otherwise, and when he has to invest his own money, he will buy the

same garbage funds that he offers to his clients.

One thing he often says is, "This fund XYZ did +20% in the last year", convincing you to sell the old fund and buy this one

(and he will take a % when you do, of course).

As we know instead, past is not future, and the next year that fund will probably do much worse than an index that

covers the market (funds that do very well for a single year are usually overexposed on a single thing, it’s just luck),

we want to have good performance over the long term.

Risk Exposure

What if overnight the market loses a good portion of its value?

From one day to the next, Gregor Samsa became an insect, suddenly, without expecting it at all.

Could this be Taleb’s famous Black Swan? :)

When investing, risk management is key to manage the unexpected things that can happen.

Stocks are by nature more volatile, although they lead to bigger gains over the long term, although not constant

(it can, for example, happen that one year they make +30% and the next year -20%), so it’s essential to keep them

in the portfolio only if you don’t necessarily expect to use them in subsequent years.

To limit fluctuations in the investment portfolio, we can add a portion of bonds with a maturity less than 5 / 10 years

(long-term bonds >10 years change a lot in price when central bank rates change).

Since bonds are designed for a shorter period, and yield less over the long term, we should see them as a way to keep

money that we may need in later years.

Bogle recommends the age rule, that as elders we should increase the % of bonds since the long-term comes less.

The formula he proposes is a % of bonds equal to 110 - age (e.g. 20 yo -> 90% stocks 10% bonds,

50 yo -> 60% stocks 40% bonds).

This rule is only indicative, and the current situation is just a personal matter, so one should not take it too

seriously: for example a 30-year-old may hold 100% stocks since he still has a whole life ahead of him.

Gregor Samsa is a stock

Gregor Samsa did everything for the family, working tirelessly to bring in the money that was needed (distributing it in dividends).

When he becomes a bug, he loses most of his value and, indeed, becomes a burden to the family, which in our comparison represents the investor. No one wants him anymore, he is hated, he tries hard to change and adapt to the new situation but fails and eventually gives up.

When he dies everyone is indifferent, which is what would happen when a company within an investment fund fails, it would simply be replaced by another stock.